A Strat a Day Episode 3 - Turn of the Month Effect

In this episode we look at a popular effect present in most asset classes, the turn of the month effect

Data

We will run this strategy on 4 different asset classes:

Stocks (SPY)

Bonds (TLT)

Real Estate (VNQ)

Commodities (GSG)

We use daily data starting 2007-06-01 and ending 2023-06-01.

You see different holding days online but the most common one I found was holding for the 4 days before the end of month and the 3 days after the end of month.

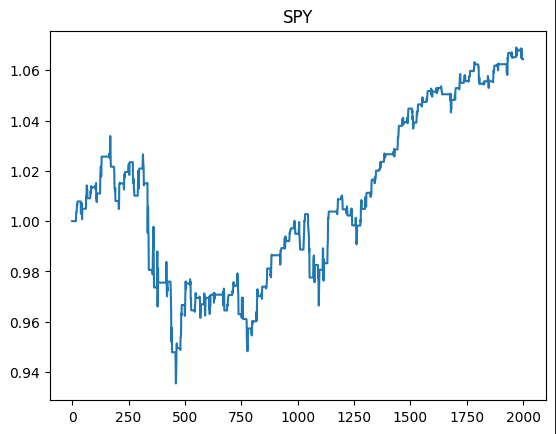

Here is how this performs (First 2000 days):

Not looking too promising yet, although we manage to get a similar performance to buy and hold while only being invested around 1/3 of the time.

Let’s break up PNL further:

Looks like none of our assets are performing really well, time for some analysis.

Analysis

The first and obvious thing to do would be to look at days around end of month and see if returns really are positive or if we see some different pattern.

That explains a lot, wee still clearly see a pattern here, things are nice and symmetric too.

TLT looks especially interesting, 1 day around end of month is super negative with all other days being positive.

Now we could try and trade those negative traders but they would be counterintuitive.

Turn of the Month effect can be explained the following way:

people get their paychecks around the end of the month and then invest into assets causing their prices to go up

So let’s trade this long only.

The trading rules will be the following:

Long SPY: 1 day from end of month and 3-7 days from end of month

Long TLT: 2-7 days from end of month

Long VNQ: 2-7 days from end of month

Long GSG: Pattern doesn’t look as nice, let’s skip it.

Here are our new results:

Nice! Looks like our new strategy is finally outperforming. Shouldn’t get your hopes up at this stage though, it’s still just in-sample. Time for the real test again:

New Strategy still outperforming Out-Of-Sample, you could argue that the old strategy is also outperforming Buy and Hold since the equity curve is much smoother. Also keep in mind it’s only invested around 1/3 of the time with same absolute pnl.

Exercise

The way this trade was explained we would expect that this effect is mostly retail driven. Could we use retail sentiment to predict returns around the end of the month?

VIX is sometimes used to gauge market sentiment. Could we use that?

Final Remarks

Tomorrows episode will be called: