Backtests Lie: Building a Stress-Test Framework for Trading Signals

Synthetic nulls, falsification audits, and backtest inflation diagnostics in Python.

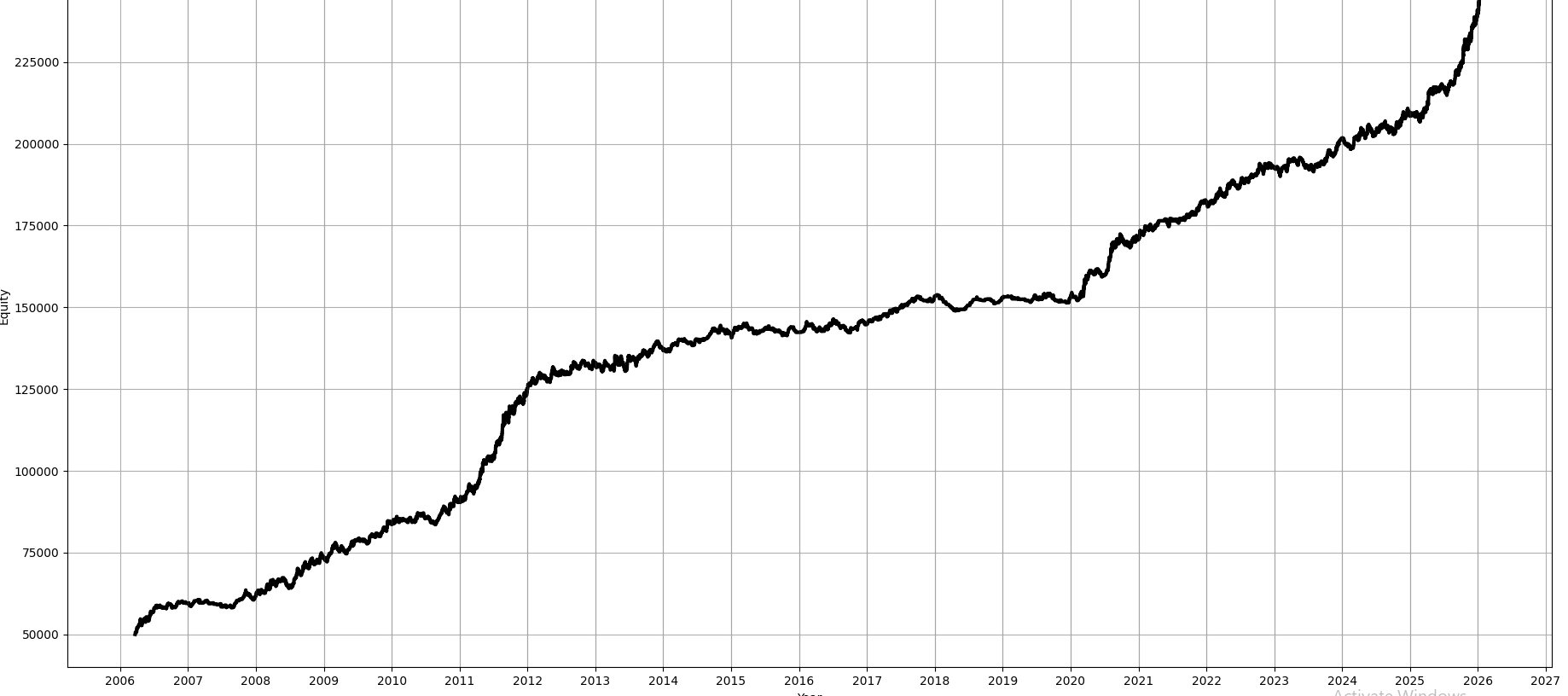

Look at this backtest I found online:

One of your first thoughts when looking at a stranger’s backtest is probably that it’s overfit, or that there is some look-ahead somewhere.

When you go a step further, you are probably constantly worried about overfitting your own backtests too!

In this article, we will introduce a framework that allows you to identify both! It’s a two-stage approach introduced in D. Nikolopoulos (2026). We will introduce the method, develop the two-stage approach, test the methodology empirically on a crypto dataset, look at some limitations, and also add some improvements of my own!

I write about quantitative trading the way it’s actually practiced:

Robust models and portfolios, combining signals and strategies, understanding the assumptions behind your models.

More broadly, I write about:

Statistical and cross-sectional arbitrage

Managing multiple strategies and signals

Risk and capital allocation

Research tooling and methodology

In-depth model assumptions and derivations

If this way of thinking resonates, you’ll probably like what I publish.