Generating Financial Data using GANs

Adversarial Training, and the TCN Architecture

When backtesting a strategy using historical data, you are limited to one sequence of events, and your backtest is essentially measuring how well your strategy fits that single path.

When pricing options using Monte Carlo methods, on the other hand, you often fit something like Brownian motion to the underlying as well as possible and take the average payoff of those simulated paths, knowing full well that they behave nothing like the real asset.

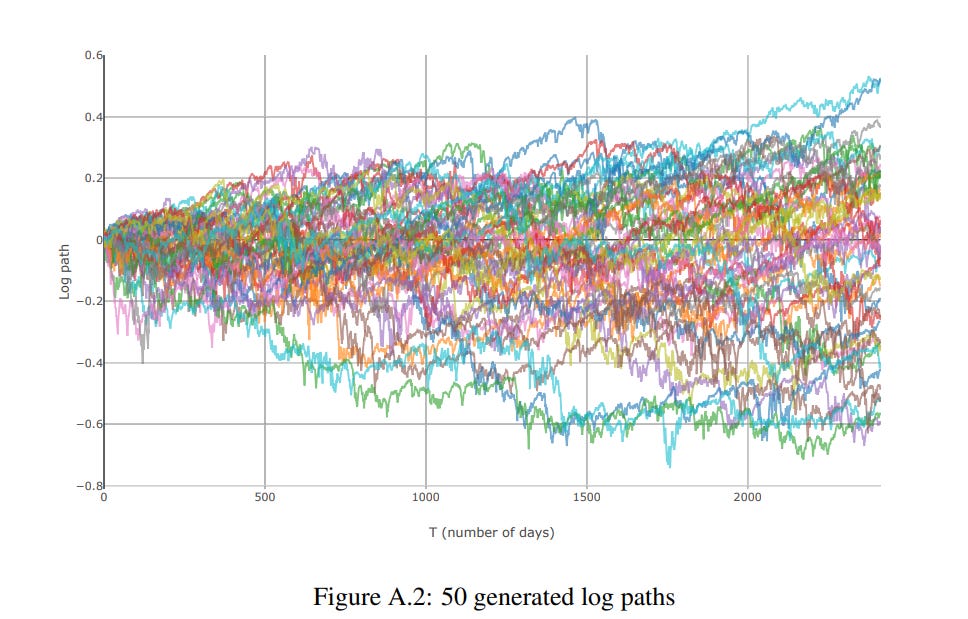

GAN's solve both of those issues by learning the data-generating process directly from real market data with no assumptions about normality, no hand-crafted volatility models, and no direct parameters. The generator learns to produce synthetic return paths that are statistically indistinguishable from the real thing, preserving heavy tails, volatility clustering, the leverage effect, etc. that are present in real markets and that parametric models consistently get wrong.

In this article, we build up the full framework from scratch. We start with the original GAN, work through the training instabilities that make it difficult to use in practice, and then introduce methods to fix this training instability. In the end, we will take a look at one specific architecture called Quant GANs that is specifically designed for financial time series.

I write about quantitative trading the way it’s actually practised:

Robust models and portfolios, combining signals and strategies, understanding the assumptions behind your models.

Topics I write about include portfolio construction, market making, risk management, research methodology, and more.

If this way of thinking resonates, you’ll probably like what I publish.

What you’ll learn

What GANs are and why they’re so hard to train in practice.

How the Wasserstein distance fixes the core mathematical failure of the original GAN objective.

How Mescheder’s gradient penalty stabilizes training.

How the Quant GAN architecture works and how it reproduces stylized facts of financial returns like heavy tails, volatility clustering, and the leverage effect.

How to evaluate a generative model for financial data, and why standard metrics like loss curves tell you almost nothing.