Event-Driven Backtester in Python

PyNL part 2!

In the previous PyNL article we’ve coded up a bunch of different risk metrics and plots.

Common Risk Metrics (PyNL Part 1)

One of the first things a new firm does is developing some research tools. You wanna make sure you can do research quickly and efficiently and be able to iterate as quickly as possible.

There is not much use to risk metrics without backtests though so in this article we will work on a more fancy kind of backtester: an event-based backtester.

We will design it in a way where switching from backtesting to trading live is super straightforward and quick.

Table of Content

For-Loop Backtester

Event-Driven Backtester

Events

Data Handler

Portfolio & Risk Manager

Execution Engine

Strategy

Performance and Monitoring

Running a Backtest

Final Remarks

For-Loop Backtester

This is the type of backtester we’ve used in all articles so far.

The general structure is:

for datapoint in data:

do_something_with_datapoint()

buy_or_sell()You always hear people talking about how amazing event-based backtesters are but for-loop backtesters actually have a couple of advantages as well.

Quick to code:

Building an event-based backtester itself takes a while and then coding up each backtest takes a while as well.

With a for-loop backtest you can much quicker test ideas and decide to throw them out of they aren’t good enough and not waste time moving on to an event-based backtest (Which you should do if the for-loop backtest comes back positive as event-based backtests are MUCH more realistic).Run faster:

Running a for-loop backtest is often a lot quicker than running an event-based one, especially if you are able to vectorize it. This can become important if you are trying to optimize a strategy via grid-search for example.

Event-Driven Backtester

With event-driven backtests we have the following general structure:

while data_vailable:

get_latest_event()

if event.type == market_data:

calculate_signal(event)

elif event.type == signal:

handle_signal(event)

elif event.type == order:

handle_order(event)

elif event.type == fill:

handle_fill(event)Different parts of the infrastructure are responsible for those different functions.

Here are the different components of the backtester itself:

Event and Event Queue:

We have market_data, signals, orders and fills as events. Those are handled and generated by the other components of the backtester and are put into a FIFO-Event Queue.Data Handler:

The data handler generates market_data events which tell the backtester that we are now looking at a new datapoint and want to do any signal calculations on that new datapoint.Portfolio & Risk Manager:

This is the heart of the event-based manager. It takes signal events from the queue and returns order events. The goal of this component is to take you from current portfolio to desired portfolio. What the desired portfolio is is also decided by this component as this is where portfolio optimizations, optimal leverage calculations etc. happen.Execution Engine:

The execution engine takes order events from the portfolio & risk manager and tries to execute them as efficiently as possible. How you want to execute an order will depend on things like how quickly it needs to be executed, what your fees are etc. Once orders are executed the execution engine will return fill events that go back to the portfolio & risk manager to make it know what our current portfolio is.Strategy:

This is self explanatory. The strategy takes market_data events, grabs the latest data from the data handler and generates signal events based on the strategy logic.Performance & Monitoring:

This component returns performance reports with performance metrics, plots etc. (Which we’ve developed in the last article).

For live systems we also want to monitor live vs. theoretical backtest results and hardware.

Now that we know the different components here is a more detailed general structure for a backtester:

events = Queue()

while True:

if data_available():

data_handler.update_data()

else:

break

while True:

if events.is_empty():

break

event = events.get()

if event.type == "MARKET":

strategy.calculate_signal(event)

portfolio.update_info(event)

elif event.type == "SIGNAL":

portfolio.handle_signal(event)

elif event.type == "ORDER":

executer.execute_order(event)

elif event.type == "FILL":

portfolio.update_cur_portfolio(event)

performance.results(portfolio)An event-based backtester has the following pros:

Eliminates look-ahead bias (mostly):

Since we are handling backtests very close to how we handle live data without indexing ([i], [i-1], [i+1], etc.) it’s much harder to accidentally introduce look-ahead bias in your backtest.Can backtest entire portfolios:

We can very easily tell the backtester what coins and what strategies we want to consider for the backtest. This gives us a much more realistic idea of what our portfolio level pnl will be in live trading.Proper portfolio management and risk management:

You most likely wouldn’t run a strategy the way you backtest it in a simple for-loop backtest. This once again makes the backtest more realistic and representative of live results.Plug & Play:

The backtester will be object-oriented.

For example if we want to switch out the execution logic in our backtest we simply use a different executer class.

Going from backtest to live should also (almost) be as easy as switching out a backtest executer class with a live executer class.

Events

First let’s code up all the different event classes in a event.py file.

We start with an interface that all events inherit from:

class Event(object):

"""

Interface for all events

"""

passMarket Event

class MarketEvent(Event):

"""

New market update

"""

def __init__(self):

self.type = "MARKET"This event doesn’t include any information besides telling the backtester that new data is available.

Signal Event

class SignalEvent(Event):

"""

Signal generated by strategy

"""

def __init__(self, symbol, timestamp, signal_type, strength):

"""

Parameters:

symbol - Ticker symbol

timestamp - Timestamp at which the signal was generated

signal_type - "LONG", "SHORT" or "EXIT"

strength - Strength of the signal

"""

self.type = "SIGNAL"

self.symbol = symbol

self.timestamp = timestamp

self.signal_type = signal_type

self.strength = strengthstrength here is a normalized signal strength since our portfolio & risk management system shouldn’t distinguish between different strategies.

It’s basically the suggested leverage from the strategy to be considered by the risk manager.

Order Event

class OrderEvent(Event):

"""

Order to be sent to execution system

"""

def __init__(self, symbol, order_type, quantity, price, direction):

"""

Parameters:

symbol - Ticker symbol

order_type - "MKT" or "LMT"

quantity - Non-negative integer for quantity

price - Quoting price (only relevant if order_type == "LMT")

direction - "LONG" or "SHORT"

"""

self.type = "ORDER"

self.symbol = symbol

self.order_type = order_type

self.quantity = quantity

self.price = price

self.direction = directionI’m keeping the order event relatively simple here without IOC and stuff like that.

You can keep adding improvements like that over time but in the beginning it’s best to start with something as simple as possible.

Fill Event

class FillEvent(Event):

"""

Filled Order returned by exchange

"""

def __init__(self, exchange, symbol, timestamp, quantity, direction, price, fees):

"""

Parameters:

exchange - Exchange where the order was filled

symbol - Ticker symbol

timestamp - Timestamp at which the order was executed

quantity - Filled quantity

direction - "LONG" or "SHORT"

price - Price at which the order was filled

fees - Fees paid/received

"""

self.type = "FILL"

self.exchange = exchange

self.symbol = symbol

self.timestamp = timestamp

self.quantity = quantity

self.direction = direction

self.price = price

self.fees = feesWhen running a strategy live you will get those variables from the exchange. When backtesting you gain them from simulation! You therefore need to make certain assumptions about fill price etc.

Data Handler

Our data handler will live in the datahandler.py file. First we make some imports:

import pandas as pd

from abc import ABCMeta, abstractmethod

from .event import MarketEventand create the following abstract class:

class DataHandler(object):

"""

Abstract interface for all data handlers (Live and Historical)

"""

__metaclass__ = ABCMeta

@abstractmethod

def get_latest_data_points(self, symbol, N=1):

"""

Returns the latest N data points from symbol (latest symbol) or fewer if less data points are available

"""

raise NotImplementedError("get_latest_data_points() not implemented!")

@abstractmethod

def update_data_points(self):

"""

Pushes the latest data point to the latest symbol for all symbols in the symbol list

"""

raise NotImplementedError("update_data_points() not implemented!")I will be implementing a datahandler that reads csv files for OHLCV data.

class HistoricalOHLCVDataHandler(DataHandler):

"""

Reads CSV files for each requested symbol

"""

def __init__(self, events, csv_dir, symbol_list):

"""

Parameters:

events - Event Queue

csv_dir - Directory path to the CSV files

symbol_list - List of symbol ticker strings

"""

self.events = events

self.csv_dir = csv_dir

self.symbol_list = symbol_list

self.symbol_data = {}

self.latest_symbol_data = {}

self.continue_backtest = True

self.open_csv_files()symbol_data here will contain the pandas dataframes for each symbol while latest_symbol_data always contains the latest datapoint for each symbol.

Now let’s implement the _open_csv_files() function which will load in all the symbols in symbol_list and save the data into pandas dataframes.

def open_csv_files(self):

"""

Opens CSV files and converts them into pandas DataFrame

"""

comb_index = None

for cur_symbol in self.symbol_list:

self.symbol_data[cur_symbol] = pd.read_csv(f"{self.csv_dir}/{cur_symbol}-OHLCV.csv").set_index("timestamp")

self.symbol_data[cur_symbol].index = pd.to_datetime(self.symbol_data[cur_symbol].index)

self.symbol_data[cur_symbol].sort_index(inplace=True)

self.symbol_data[cur_symbol] = self.symbol_data[cur_symbol].loc[~self.symbol_data[cur_symbol].index.duplicated(keep='last')]

if comb_index is None:

comb_index = self.symbol_data[cur_symbol].index

else:

comb_index.union(self.symbol_data[cur_symbol].index)

self.latest_symbol_data[cur_symbol] = []

for cur_symbol in self.symbol_list:

self.symbol_data[cur_symbol] = self.symbol_data[cur_symbol].reindex(

index=comb_index, method="ffill"

)

self.symbol_data[cur_symbol] = self.symbol_data[cur_symbol].iterrows()And next the _get_new_bar() function which gives us the latest data point (here a bar) as a tuple:

def get_new_bar(self, symbol):

"""

Returns the latest bar from the data feed as a tuple

(symbol, timestamp, open, high, low, close, volume)

"""

for bar in self.symbol_data[symbol]:

yield tuple([symbol, bar[0].timestamp(), bar[1]["open"], bar[1]["high"], bar[1]["low"], bar[1]["close"], bar[1]["volume"]])We use yield here instead of return to create a generator for the latest data point.

Using those 2 helper functions we can now code up the 2 abstract functions that need to be implemented in every data handler.

def get_latest_data_points(self, symbol, N=1):

try:

bars_list = self.latest_symbol_data[symbol]

except KeyError:

print("{symbol} data not available!")

else:

return bars_list[-N:]def update_data_points(self):

for cur_symbol in self.symbol_list:

try:

bar = next(self.get_new_bar(cur_symbol))

except StopIteration:

self.continue_backtest = False

else:

if bar is not None:

self.latest_symbol_data[cur_symbol].append(bar)

self.events.put(MarketEvent())Portfolio & Risk Manager

For this component we create a new python file portfolio.py with the following imports:

import pandas as pd

from abc import ABCMeta, abstractmethod

from .event import OrderEventand the following abstract class:

class Portfolio(object):

"""

Handles positions and fills creating new Orders

"""

__metaclass__ = ABCMeta

@abstractmethod

def update_signal(self, event):

"""

Generates new Order from SignalEvent

"""

raise NotImplementedError("update_signal() not implemented!")

@abstractmethod

def update_fill(self, event):

"""

Updates current Portfolio based on FillEvent

"""

raise NotImplementedError("update_fill() not implemented!")I’ll be implementing a very naive portfolio and risk manager that blindly generates orders for all signals that it gets with size equal to the signal strength.

class NaivePortfolio(Portfolio):

"""

Naive Portfolio Manager that sends orders with constant quantity blindly

without any risk management or position sizing

"""

def __init__(self, bars, events, start_date, initial_capital=100000.0):

"""

Parameters:

bars - DataHandler object with current market data

events - Event Queue object

start_date - Start date of the portfolio

initial_capital - Starting capital in USD

"""

self.bars = bars

self.events = events

self.start_date = start_date

self.initial_capital = initial_capital

self.symbol_list = self.bars.symbol_list

self.all_positions = self.construct_all_positions()

self.current_positions = dict((k, v) for k,v in [(cur_symbol, 0) for cur_symbol in self.symbol_list])

self.all_holdings = self.construct_all_holdings()

self.current_holdings = self.construct_current_holdings()all_positions and all_holdings contain all the historical portfolio positions and holdings (cash, total portfolio value, etc.)

def construct_all_positions(self):

"""

Constructs the positions list using the start_date

to determine when the time index will begin

"""

d = dict((k,v) for k, v in [(cur_symbol, 0) for cur_symbol in self.symbol_list])

d["timestamp"] = self.start_date

return [d]def construct_all_holdings(self):

"""

Constructs the holdings list using the start_date

to determine when the time index will begin

"""

d = dict((k,v) for k, v in [(cur_symbol, 0) for cur_symbol in self.symbol_list])

d["timestamp"] = self.start_date

d["cash"] = self.initial_capital

d["fees"] = 0.0

d["total"] = self.initial_capital

return [d]def construct_current_holdings(self):

"""

Construcs the dictionary which will hold the instantaneous

value of the portfolio across all symbols

"""

d = dict((k,v) for k, v in [(cur_symbol, 0) for cur_symbol in self.symbol_list])

d["cash"] = self.initial_capital

d["fees"] = 0.0

d["total"] = self.initial_capital

return dNow we will implement a function that updates our positions and holdings if a new data point appears:

def update_market(self):

"""

Adds a new record to the positions and holdings matrices for the current market data bar.

Uses MarketEvent from events queue.

"""

bars = {}

for cur_symbol in self.symbol_list:

bars[cur_symbol] = self.bars.get_latest_data_points(cur_symbol, N=1)

# Update positions

dp = dict((k,v) for k, v in [(cur_symbol, 0) for cur_symbol in self.symbol_list])

dp["timestamp"] = bars[self.symbol_list[0]][0][1]

for cur_symbol in self.symbol_list:

dp[cur_symbol] = self.current_positions[cur_symbol]

self.all_positions.append(dp)

# Update holdings

dh = dict((k,v) for k, v in [(cur_symbol, 0) for cur_symbol in self.symbol_list])

dh["timestamp"] = bars[self.symbol_list[0]][0][1]

dh["cash"] = self.current_holdings["cash"]

dh["fees"] = self.current_holdings["fees"]

dh["total"] = self.current_holdings["cash"]

for cur_symbol in self.symbol_list:

market_value = self.current_positions[cur_symbol] * bars[cur_symbol][0][5]

dh[cur_symbol] = market_value

dh["total"] += market_value

self.all_holdings.append(dh)Next we need 2 functions that update our current positions and current holdings if we get back a fill from the execution engine:

def update_positions_from_fill(self, fill):

"""

Updates the positions according to a FillEvent

Parameters:

fill - FillEvent object

"""

fill_dir = 0

if fill.direction == "LONG":

fill_dir = 1

if fill.direction == "SHORT":

fill_dir = -1

self.current_positions[fill.symbol] += fill_dir*fill.quantitydef update_holdings_from_fill(self, fill):

"""

Updates the holdings according to a FillEvent

Parameters:

fill - FillEvent object

"""

fill_dir = 0

if fill.direction == "LONG":

fill_dir = 1

if fill.direction == "SHORT":

fill_dir = -1

fill_price = self.bars.get_latest_data_points(fill.symbol)[0][5]

cost = fill_dir * fill_price * fill.quantity

self.current_holdings[fill.symbol] += cost

self.current_holdings["fees"] += fill.fees

self.current_holdings["cash"] -= cost + fill.fees

self.current_holdings["total"] -= cost + fill.feesTo not type out both functions each time we get a fill we create another function that simply runs both of those functions (one of the 2 abstract classes):

def update_fill(self, event):

if event.type == "FILL":

self.update_positions_from_fill(event)

self.update_holdings_from_fill(event)Next the naive order creation:

def generate_naive_order(self, signal):

"""

Creates OrderEvent with constant quantity (100) using signal

Parameters:

signal - SignalEvent object

"""

order = None

symbol = signal.symbol

signal_type = signal.signal_type

strength = signal.strength

mkt_quantity = strength

cur_quantity = self.current_positions[symbol]

order_type = "MKT"

if signal_type == "LONG" and cur_quantity == 0:

order = OrderEvent(symbol, order_type, mkt_quantity, None, "LONG")

if signal_type == "SHORT" and cur_quantity == 0:

order = OrderEvent(symbol, order_type, mkt_quantity, None, "SHORT")

if signal_type == "EXIT" and cur_quantity > 0:

order = OrderEvent(symbol, order_type, abs(cur_quantity), None, "SHORT")

if signal_type == "EXIT" and cur_quantity < 0:

order = OrderEvent(symbol, order_type, abs(cur_quantity), None, "LONG")

return orderand the last abstract function that takes the order created by generate_naive_order() and puts it in the queue:

def update_signal(self, event):

if event.type == "SIGNAL":

order_event = self.generate_naive_order(event)

self.events.put(order_event)Execution Engine

Next is the (very simple) execution engine in execution.py:

import datetime

from abc import ABCMeta, abstractmethod

from .event import FillEventclass ExecutionHandler(object):

"""

Abstract interface for Execution Engines responsible for

executing trades

"""

__metaclass__ = ABCMeta

@abstractmethod

def execute_order(self, event):

"""

Takes and Order event and executes it producing a Fill event

Parameters:

event - Event object with order information

"""

raise NotImplementedError("execute_order() is not implemented!")Our execution engine will just convert orders into the respective fills without returning a fill price as our portfolio & risk manager already assumes we get filled at the close.

class SimulatedExecutionHandler(ExecutionHandler):

"""

Converts all Order objects into their equivalent Fill objects

without any latency, slippage, etc.

"""

def __init__(self, bars, events):

"""

Parameters:

bars - DataHandler object that provides bar information

events - Queue of Event objects

"""

self.bars = bars

self.events = events

def execute_order(self, event):

"""

Parameters:

events - Event object with order information

"""

if event.type == "ORDER":

fill_event = FillEvent("TestExchange", event.symbol, datetime.datetime.now().timestamp(),

event.quantity, None, event.direction, 0.0003*event.quantity*self.bars.get_latest_data_points(event.symbol)[0][5])

self.events.put(fill_event)I’ve hard coded 3bps as a fee here.

Strategy

Now for our strategies in strategy.py:

from abc import ABCMeta, abstractmethod

from .event import SignalEventclass Strategy(object):

"""

Abstract interface for all strategies

"""

__metaclass__ = ABCMeta

@abstractmethod

def calculate_signals(self):

"""

Calculates list of signals

"""

raise NotImplementedError("calculate_signals() not implemented!")The strategy that we will implement is a simple buy and hold.

It will send a buy signal for each instrument and then never sell.

class BuyAndHoldStrategy(Strategy):

"""

Goes LONG all of the symbols as soon as a bar is received.

"""

def __init__(self, bars, events):

"""

Parameters:

bars - DataHandler object that provides bar information

events - Event Queue object

"""

self.bars = bars

self.symbol_list = self.bars.symbol_list

self.events = events

self.bought = self.calculate_initial_bought()bought is a dictionary that tells us if we already bought an instrument or not.

calculate_inital_bought() simply sets every value to False.

def calculate_initial_bought(self):

"""

Creates dictionary with symbols as keys with all set to False

"""

bought = {}

for cur_symbol in self.symbol_list:

bought[cur_symbol] = False

return boughtWe now implement the abstract class that actually calculates the signal:

def calculate_signals(self, event):

if event.type == "MARKET":

for cur_symbol in self.symbol_list:

bars = self.bars.get_latest_data_points(cur_symbol, N=1)

if bars is not None and bars != []:

if self.bought[cur_symbol] == False:

signal = SignalEvent(bars[0][0], bars[0][1], "LONG", 1.0)

self.events.put(signal)

self.bought[cur_symbol] = TruePerformance and Reporting

This is the last component of our simple event-based backtester! It will be in performance.py.

import pandas as pd

from abc import ABCMeta, abstractmethod

from . import metrics_and_plots as mpmetrics_and_plots contains our risk metrics and plots that we’ve coded in the previous PyNL article.

class Performance(object):

"""

Handles performance reports and monitoring

"""

__metaclass__ = ABCMeta

@abstractmethod

def report(self, event):

"""

Returns a performance report

"""

raise NotImplementedError("report() not implemented!")Our implementation will return every performance metric and plot that we’ve coded up:

class SimplePerformanceReport(Performance):

"""

Returns basic performance statistics and plots

"""

def __init__(self, portfolio):

"""

Parameters:

portfolio - Portfolio and Risk Manager containing the portfolio to be analyzed

"""

self.portfolio = portfolio

self.summary = pd.DataFrame()

def create_equity_curve_dataframe(self):

"""

Creates a pandas DataFrame from the all_holdings list of dictionaries

"""

summary = pd.DataFrame(self.portfolio.all_holdings).set_index("timestamp")

summary["returns"] = summary["total"].pct_change()

summary["equity"] = (1.0+summary["returns"]).cumprod()

self.summary = summary

def summary_statistics(self):

"""

Outputs a bunch of performance statistics for the equity curve

"""

pd.set_option('display.max_columns', None)

print(self.summary)

alpha = 0.05

T = (self.summary.index[-1] - self.summary.index[0])/(60*60*24*365)

equity = self.summary["equity"].values[1:]

sharpe_ratio = mp.metrics.sharpe_ratio(equity, T)

sortino_ratio = mp.metrics.sortino_ratio(equity, T)

calmar_ratio = mp.metrics.calmar_ratio(equity, T)

max_drawdown = mp.metrics.max_drawdown(equity)

omega_ratio = mp.metrics.omega_ratio(equity)

VaR = mp.metrics.VaR(equity, alpha)

CVaR = mp.metrics.CVaR(equity, alpha)

print(f"Sharpe Ratio: {sharpe_ratio}")

print(f"Sortino Ratio: {sortino_ratio}")

print(f"Calmar Ratio: {calmar_ratio}")

print(f"Maximum Drawdown: {max_drawdown}")

print(f"Omega Ratio: {omega_ratio}")

print(f"Value at Risk ({alpha*100}%): {VaR*100}%")

print(f"Conditional Value at Risk ({alpha*100}%): {CVaR*100}%")

mp.plots.plot_drawdown(equity)

mp.plots.plot_return_cdf(equity, show=True)I’ve made a little change to plot_drawdown and plot_return_cdf:

if show:

plt.show()Adding this at the end allows me to do multiple plots in the report without having to import matplotlib and doing plt.figure() etc.

And with that our event-based backtester is finally complete! Let’s use it to do an actual backtest now!

Running a Backtest

I’ve already done most of the work in the pseudo-code in the Event-Based Backtester section of the article.

Now we just need to convert the pseudo-code to real code:

import infrastructure

from queue import Queue

symbols = ["BNBUSDT", "BTCUSDT"]

event_queue = Queue()

datahandler = infrastructure.datahandler.HistoricalOHLCVDataHandler(event_queue, "C:/QuantData/OHLCV/Binance", symbols)

portfolio = infrastructure.portfolio.NaivePortfolio(datahandler, event_queue, 1690934400)

executionengine = infrastructure.execution.SimulatedExecutionHandler(datahandler, event_queue)

buyandhold = infrastructure.strategy.BuyAndHoldStrategy(datahandler, event_queue)

performance = infrastructure.performance.SimplePerformanceReport(portfolio)

while True:

if datahandler.continue_backtest == True:

datahandler.update_data_points()

else:

break

while True:

try:

event = event_queue.get(False)

except:

break

else:

if event is not None:

if event.type == "MARKET":

buyandhold.calculate_signals(event)

portfolio.update_market()

elif event.type == "SIGNAL":

portfolio.update_signal(event)

elif event.type == "ORDER":

executionengine.execute_order(event)

elif event.type == "FILL":

portfolio.update_fill(event)

performance.create_equity_curve_dataframe()

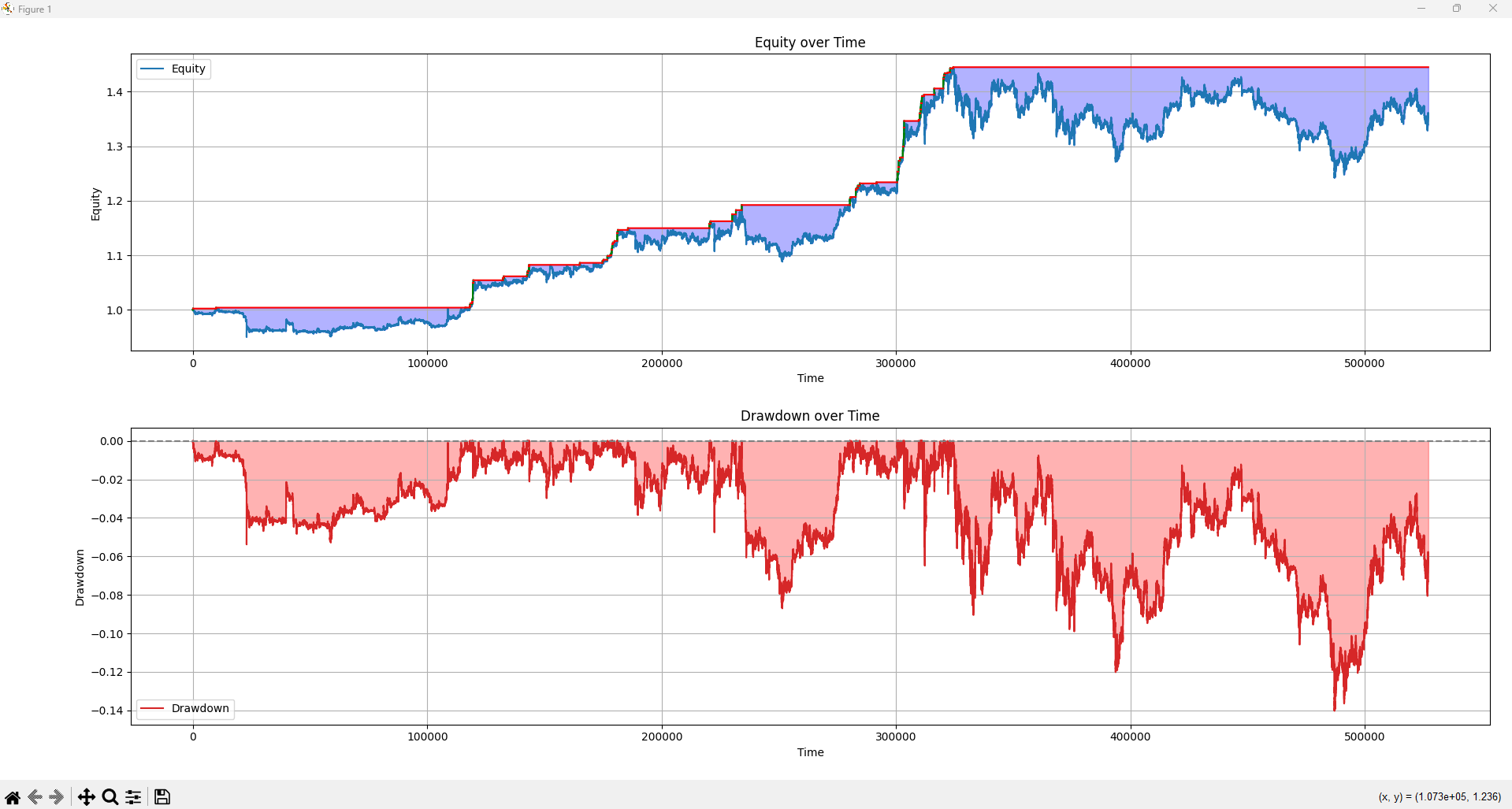

performance.summary_statistics()We get back the following report:

Final Remarks

Just 2 articles later and PyNL is already starting to become a pretty useful library!

You could already use this event-based backtester to run simple backtests.

With this backtester the sky is the limit, you can introduce volatility forecasting to the risk manager, add portfolio optimization techniques, implement execution algorithms like VWAP and TWAP etc.

Implement whatever you need and which will allow you to efficiently backtest strategies!

Thx for sharing!

Would you recommend to use an off the shelf backtesting framework (E.g. vectorbt pro/ backtesting.py) or writing our own?

Hey Vertox is there a GitHub repo I can follow along? Thanks in advance